This article originally appeared in the May 6 issue of Birmingham Medical News.

Check-ups, tests, and results. Doctors provide, measure, and deliver data to patients every day, often with profound implications. Financial advisors, at least the diligent ones, offer the same to their clients. Much of our data focuses on helping people have confidence that they can do what they want to do and not run out of money at the same time. Approaches and technical tools may vary, often with significant differences in degrees of sophistication. It has been common practice for advisors to use these tools to help project a portfolio’s ability to provide income for retirement. Rates of return are calculated, spending requirements input, withdrawal rates assumed, and end-of-life portfolio values projected. Seemingly less commonly do financial planning practitioners employ analytical tools that attempt to address the impact that random rates of return can have on account levels and the resulting implied long-term financial health of the client. As most experienced investors may know, we don’t always enjoy the average rate of return, even over extended lengths of time. Banking on a historical average and ignoring the potential threat that a series of lower than expected returns can have on a portfolio could reduce the life expectancy of the portfolio, and the unaware investor could find oneself surprised and on the way to running out of money, with few options available to alter the outcome. By introducing random returns, Monte Carlo analysis attempts to alleviate this problem.

Monte Carlo Analysis

So what is Monte Carlo Analysis? Simply put, it is an attempt to examine the likelihood of potential outcomes, based on random inputs. With respect to retirement planning, random returns based on historical volatility and performance measures are applied to a portfolio over the course of an investor’s life expectancy. This is not done once, but at least one thousand times. The results offer a potential range of portfolio values at the end of one’s life expectancy, and the investor is given an opportunity to more clearly define the impact of current decisions.

The chart below was produced by our planning software. We use eMoney, but other programs are available. This is a hypothetical illustration and is used for demonstration purposes.

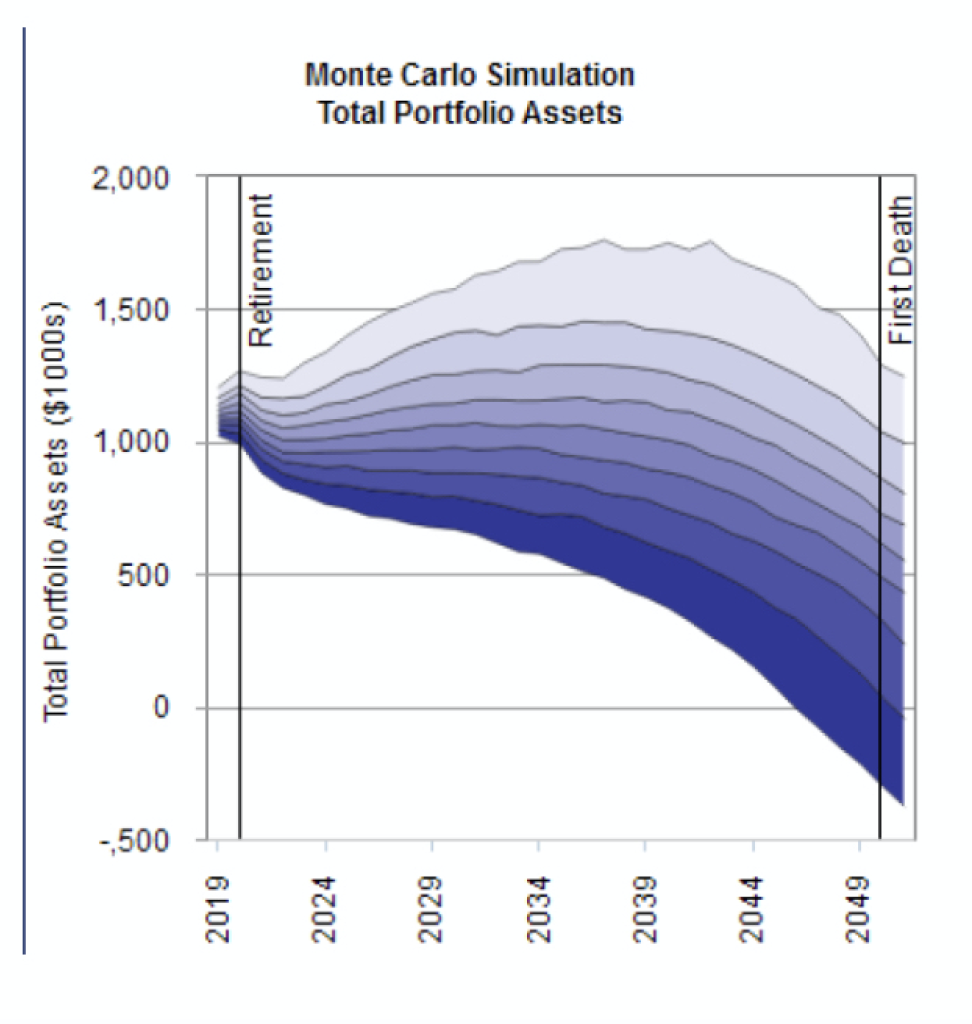

This graph draws the distinction between average and random returns. Here we have a couple close to retirement with an investment portfolio valued at approximately $1 million. Using the average rate of return, after factoring in household income spending, pension, and social security income sources, and inflation, this household is projected to have almost $700,000 at age 95. Granted, inflation may reduce the purchasing power of this figure, but at age 95, this is a projection that many investors on the verge of retirement might find acceptable.

These Monte Carlo results reflect the same assumptions but introduce random rates of return. Given a life expectancy assumption of age 95 for both spouses, we see final portfolio values for the younger spouse in her last year:

The blue border at the bottom marks the tenth percentile. At first glance, it looks like this portfolio declines to zero around 20 percent of the time. If your odds were almost one out of five that your investment portfolio would shrink to nothing, even though the average outcome has you close to $700,000, wouldn’t you want to know, and wouldn’t you want the opportunity to do something about it? Some readers might elect to work longer, find a part-time job, or re-allocate the portfolio, in hopes of obtaining a better return. Others may assume the risk, hope for the best, and know that in the future some belt-tightening might be likely. The point is, wouldn’t it be good to know beforehand, what the odds were?

This tool may be applied to a myriad of scenarios–premature death and its impact on the surviving spouse, whether or not one can afford to self-insure against long term care costs, buying a vacation home, choosing the most appropriate school, or increasing the travel budget. Monte Carlo analysis may be used to help investors make better decisions, and to have more confidence when they make them.

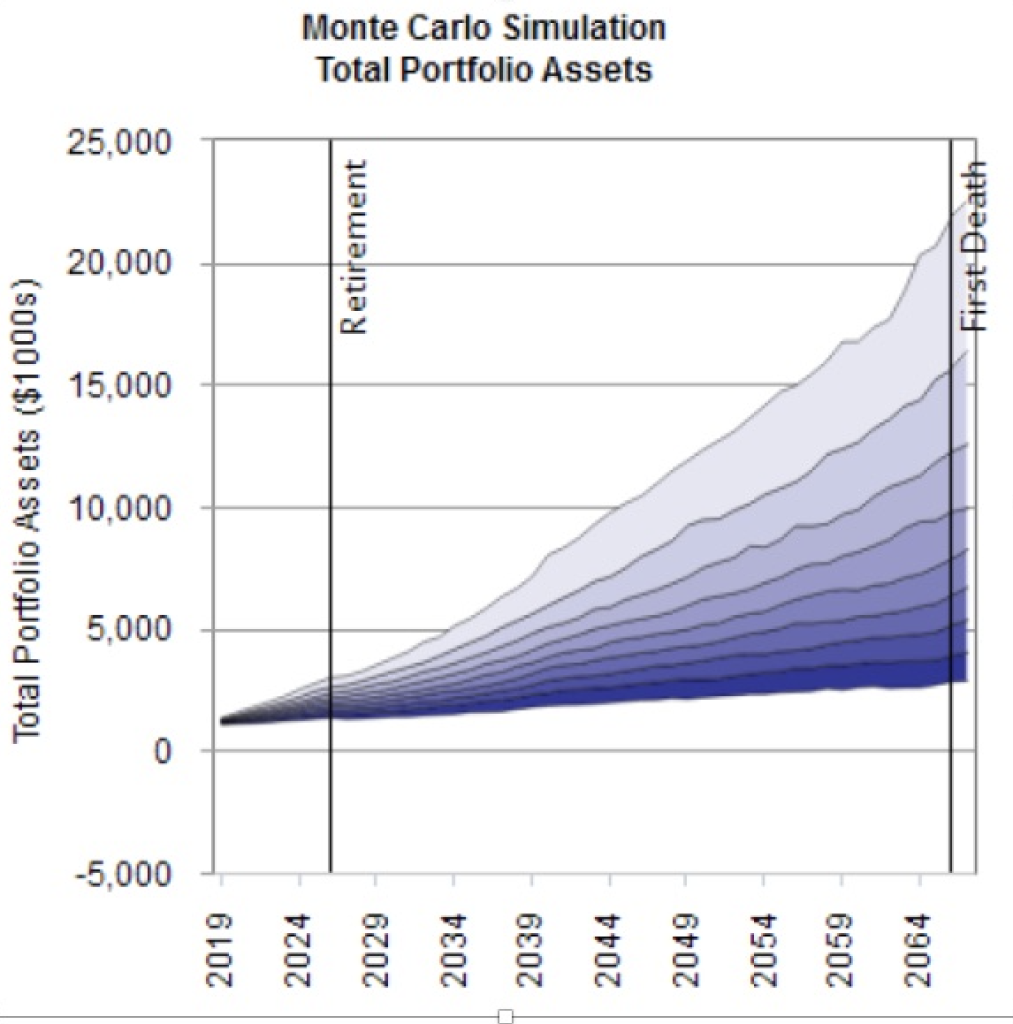

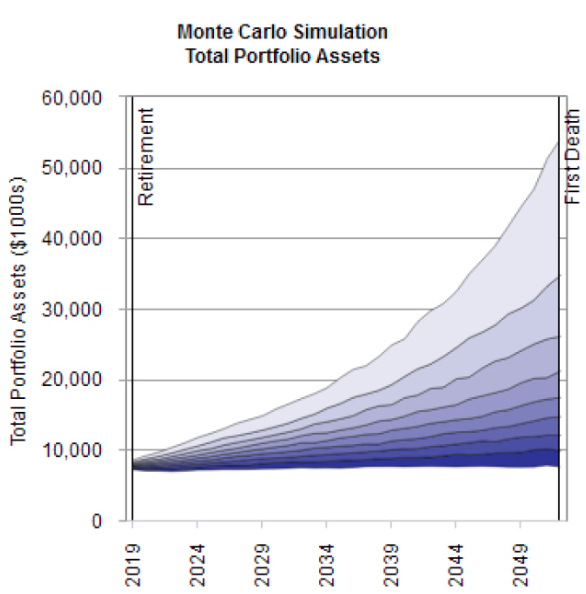

Too, it should be noted, even stressed, that Monte Carlo Analysis doesn’t always result in recommended belt-tightening. Sometimes, in cases such as the two below, we might encourage clients to spend more money, enjoy the thought of their children’s inheritance, give more freely to their charities, or, even, just relax.

Just as every patient should have a routine physical, so should every investment portfolio have a routine review. Just as blood pressure, heart rate, cholesterol, and the like should be analyzed in the former, so should Monte Carlo Analysis be performed in the latter. Without it, the picture is incomplete.

Bridgeworth, LLC is a registered investment adviser.

This material is not to be construed as an offer to sell or a solicitation of an offer to buy any security. Investing in any security or investment strategies discussed herein may not be suitable for you, and you may want to consult a financial advisor. Nothing in this material constitutes individual investment, legal or tax advice. Investments involve risk and an investor may incur either profits or losses.

Bridgeworth, LLC shall accept no liability for any loss arising from the use of this material, nor shall Bridgeworth, LLC treat any recipient of this material as a customer or client simply by virtue of the receipt of this material.

Investing in stock includes numerous specific risks including the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Past performance should not be taken as an indication or guarantee of future performance. There is no guarantee that any forecasts made will come to pass.

2.881892.0419