Our unwelcome foe, market volatility, decided to return in the first quarter of 2018. Many financial advisors have reminded clients that “the stock market is volatile”; an undeniable fact of investing. In actuality, it is this risk that drives away some and attracts a smaller subset of investors, providing the opportunity for the return we seek. Said another way, if people could buy a “safe, non-volatile asset” with a 10% return, everyone would want it and would bid up the price until it yielded something much less attractive. Of course, the opposite is also true … the more volatile and less probable a return, there would be fewer buyers and thus a lower price for the asset, leading to the potential for a much higher return. So while we prefer to have high-returning and low-volatility assets, the two characteristics are polar opposites in many ways; therefore, we consider the role of an investment professional is to diversify the risks and build a portfolio that has the possibility to meet your return objective, while also not having so much risk that clients get scared out of their positions, and their portfolios, before they work towards achieving their intended objective. What makes this past quarter’s ups and downs feel possibly worse than they actually are is in part because the past year and a half has not had any drops of more than 5%, while on average over the last 38 years there has been one 10% drop and four 5% magnitude drops per year. While we do not cheer the return of volatility and recognize that we might experience even more volatility than we have been accustomed to, we also feel it isn’t necessarily the sign of the end of a bull market, but rather a regular part of the investing experience.

US Stocks

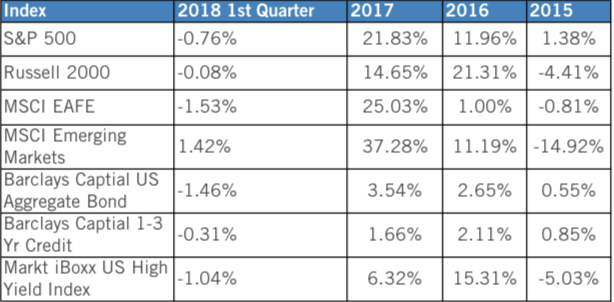

In January, the bull market was still raging from 2017 and the S&P 500 was up over 7%. As we rolled into February, strong economic data spurred fears of inflation and interest rate hikes, resulting in a rapid turnaround and some heavy days of selling. This can be confusing, but yes, sometimes good economic news can mean bad news for stocks. Market volatility can go in both directions and some big “up” days followed, as investors tried to digest new information and form a new consensus view of where the markets were headed. March ended with two main drivers taking the indices back lower: fears of trade wars and trouble in a few large technology stocks.

So what now? It’s important to try to focus on the majors and not get lost in one-off situations or factors which may not change the larger narrative. While the current bull market and economic cycle might be approaching the later stages, economic growth and earnings growth in the nearer term appear strong. Certainly, investors get more skittish as they fear that there is an eventual end to the bull market, but that eventual end could be one year, maybe two, or possibly more away, and every downturn doesn’t have to mean that another 2008 has arrived. Secondly, keep in mind that trade “talks” are just that as of now, no real policies have been cemented. J.P. Morgan’s Chief Investment Strategist David Kelly suggest we are much more likely talking “trade skirmishes” rather than “trade wars”. The U.S. and many other major countries all have a co-dependent relationship (they need us and we need them), which keeps actual policy less dramatic than rhetoric spewed by both sides. One should be careful in speculating about how it will all fall out as there are many moving pieces. As for the tech giants that have come under pressure, it’s a reminder that no company, not even tech companies that are changing the world, is immune from various risks and pressures. Finally, despite the wild ride, the S&P 500 ended the quarter down 0.76%, but because of increased analyst expectations on earnings (in large part caused by corporate tax cuts), the valuation of the S&P 500 came back down to nearly the 25-year average (PE ratio of 16.4 vs. 16.1). So, the backdrop for U.S. stocks is actually pretty good in the nearer term, but also recognize that we might need to grow some thicker skin to handle volatility.

International Stocks

As value investors, we cheered the 25.03% in the EAFE Index (representing developed-market international stocks) last year; it was long awaited. If you want to know the market action in international stocks, it was nearly identical to its U.S. counterparts, following the ups and downs we experienced. There are a few lessons here, but one of the primary ones is that international stocks, in general, can be highly correlated to the U.S. market. This is in part because so many large U.S. companies have a global footprint and because it’s the same investors who buy them both, so when “scared”, it appears they often don’t discriminate in their selling. While the EAFE index ended the quarter down 1.53%, the outlook highlighted in our year-end review is still intact. Economic growth is strong, unemployment continues to decline, corporate profits are improving, and valuations of stocks are attractive. Because stock markets can be correlated, it’s unclear if last year’s bull market is still running or could be stalled if U.S. stocks struggle. A U.S. trade war, even with China, could tamper global growth which Europe is highly sensitive to, but as stated, we are hoping for a skirmish rather than something profound. As investors, we believe that diversification alone is a solid reason for owning international stocks but that improved fundamentals and valuation make for an even stronger case. A challenge for many investors is that lackluster performance of international stocks, in comparison to the tremendous returns in U.S. stocks in recent years causes one to question if they can produce going forward. This is where we choose to rely on math and fundamentals and not our emotions as we allocate for the future.

Emerging Markets

A quick turn of the channel will probably result in some headline regarding an “emerging market” country, namely China or Mexico. These trade “discussions” have started with the U.S. suggesting tariffs to correct what is deemed unfair trade deals and practices by various countries. Of course, as you would expect, nobody likes being accused of wrong-doing or the status quo changing and the dialogue/rhetoric on all sides has ramped up. I think the key takeaway is to remember this co-dependency mentioned previously and hope that what Adam Smith, the father of modern economics, called rational self-interest will prevail. This idea is that the best outcome is achieved when people act in their own self-interest, a sort of equilibrium is attained when people realize they can’t get all they want and in order to get some of what they want, they have to bend a little. This isn’t always a pretty process and not all actors may be rational at all times, but I think it is a fair assumption. Economic and corporate earnings growth has been strong in Emerging Markets and the index finished the quarter the highest of any equity market, up 1.42%.

Bonds

The world of bonds in comparison to stocks is normally pretty boring. Unlike stocks which are highly volatile, bonds due to their very structure don’t usually provide a lot of excitement. On top of that, interest rates for decades have been declining, making most “surprises” for bond investors positive ones. A few recent changes have made this year a bit different. First, the Federal Reserve has been slowly raising interest rates over the last few years and raised another 0.25% in March, with another two to three hikes probable. This is a slight headwind for bond investors, but much of this information is accounted for in current bond prices. Secondly, for what it is worth, we have a new Chairman of the Federal Reserve, Jerome “Jay” Powell, to replace Janet Yellen. This changing of the guard always takes some getting used to, but unlikely to be a big change. Jay, unfortunately, started on the job Feb 5, which was right in the middle of the stock market dropping and bond prices dropping/rates rising; welcome Jay! While rate increases by the Fed are a negative for bond holders, we also know that with volatility in stocks on the rise, we should be careful to not abandon a critical diversifier for our portfolios. The universe for bonds is very large and we aim to navigate the puzzle of portfolio construction recognizing that a truly diversified portfolio means that something in your portfolio is likely to be disappointing and in fact, if everything is working at the same time, you probably aren’t really diversified. Our goal is to minimize the magnitude of any disappointing asset classes and focus on the overall result over time. The U.S. Aggregate bond index ended the quarter -1.46% and the high yield bond index returned -1.04%.

Are We Having Fun Yet?

Nobody ever said investing was easy and I think today’s environment is a perfect example of an emotionally risky situation for individual investors. What I mean is that it seems that the news cycle is constantly negative, political rhetoric is high, several big geopolitical items are at the forefront of peoples’ minds, and the stock market has been very good for a period of time and certainly last year. This environment makes most individuals a little nervous, which is understandable. However, the economic and company data points that don’t make the evening news are likely to be what drives markets. The old saying “it’s difficult to make predictions, especially about the future” still holds true, but this has always been the case for investors. As investors, our job is to remove emotion, stick to our process, and remain patient when investing capital. It is not always easy to do, but we are confident that together, the team at Bridgeworth, with your cooperation, can keep striving towards your precious goals. We appreciate your trust in us as a steward of your capital.

BTN# 1-717951.0418

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 5, 2018, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Bridgeworth, LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not ensure against market risk.

Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass.

Reliance upon information in this material is at the sole discretion of the reader.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

International investing involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments.

The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments.

Any securities, indices, and other financial benchmarks shown are provided for illustrative purposes only, and reflect reinvestment of income, dividends, and other earnings. They do not reflect the deduction of advisory fees. Investment products are subject to investment risk, including possible loss of the principle amount invested. You cannot invest directly in an index.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following developed country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

The MSCI EM (Emerging Markets) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the emerging market countries of the Americas, Europe, the Middle East, Africa and Asia. The MSCI EM Index consists of the following emerging market country indices: Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Egypt, Greece, Hungary, Poland, Qatar, Russia, South Africa. Turkey, United Arab Emirates, China, India, Indonesia, Korea, Malaysia, Philippines, Taiwan, and Thailand.

The Bloomberg Barclays U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

Barclays 1-3 Year Government Bond – Barclays 1-3 Year Government Bond Index is a market value-weighted performance benchmark of investment grade government and corporate bonds with maturities of one to three years.

The Markit iBoxx USD Liquid High Yield Index is designed to reflect the performance of USD denominated high yield corporate debt. The index rules aim to offer a broad coverage of the USD high yield liquid bond universe. The Markit iBoxx USD Liquid High Yield Index is rebalanced once a month at the month-end (the “rebalancing date”) and consists of sub-investment grade USD denominated bonds issued by corporate issuers from developed countries and rated by at least one of three rating services: Fitch Ratings, Moody’s Investors Service, or S&P Global Ratings.

Neither Bridgeworth nor its content providers are responsible for any damages or losses arising from any use of this information. To determine which investments may be appropriate for you, consult your financial advisor prior to investing.

Securities sold by Bridgeworth Financial advisors are offered through LPL Financial, Member FINRA/SIPC. Investment advice is offered through Bridgeworth, LLC, SEC Registered Investment Advisor. Bridgeworth Financial and Bridgeworth, LLC are separate entities from LPL Financial.