Radio and TV advertisements might have you believe that owning gold keeps you safe from a myriad of issues (i.e., a growing government deficit, geopolitical risk, and inflation, just to name a few), but should you really own gold? In your decision to own or not own gold, you first must define your threat model and weigh how much this threat means to you. Three common threat models that come to mind when deciding to own gold are 1) cataclysmic disaster, 2) portfolio capital preservation against inflation, and 3) a hedge against disruptive financial circumstances.

A cataclysmic disaster threat model includes events such as nuclear war, a human race-ending pandemic, artificial intelligence like ChaosGPT tasked to “destroy humanity,” or any other catastrophic event that would force us back to the bartering system. The probability of these types of events is low, but they are not zero and are a shared concern by some, including those who have found “prepping” as a fun hobby. In this threat model, owning gold as an asset, not an investment derivative, is sensible as it can be used for bartering (assuming it holds perceived value). One might suggest stocking up ammo, cigarettes, liquor, and seeds, as these may hold more value in the end times. Acquiring physical gold can be intimidating and challenging to new buyers due to its fragmentation, but I would recommend talking with your local dealer and comparing their price to the spot gold price online. For practical reasons, gold coins would be favorable over gold bars, but you can often find a better price on gold bars. Gold jewelry is another option that also has fashion utility. Physical gold can have significant monetary value at times, so safe storage is also an important consideration when acquiring physical gold. A home safe or storing in a bank safety deposit box would be advisable for extensive physical holdings of gold. For probability reasons I stated before, this is not a threat model basket I would put all my eggs in, but if the value of this threat is important to you, then owning gold and “prepping” might be something for you to explore.

Capital preservation against inflation is a second threat model an individual may use when considering owning gold. No one wants the value of their hard-earned dollar to be eroded away by inflation, and this has been a top concern for many investors as of late, with the Consumer Price Index (CPI) up 5.6% year-over-year in March 2023. A commonly held belief is that gold acts as a hedge to inflation (or rises more than inflation) during inflationary periods. Many with this belief point to the six years between 1973 and 1979 when average annual inflation was up around 8%, and gold’s annual return was 34% [2]. Still, gold’s more recent historical performance tells a different story. The yearly average inflation from 1980 to 1984 was around 7.5%, but gold prices fell 10% annually [2]. Again in 1988-1991, annual inflation averaged about 4.6%, but gold prices fell approximately 7.6% a year on average [2]. Most recently, in 2022, CPI rose 6.5% annually, though gold only rose approximately 0.44% annually [2]. Despite what many believe, gold’s track record as an inflation hedge is less reliable. Investors should consider other options, such as owning equities, real estate, or commodities, if inflation is a top concern in their threat model.

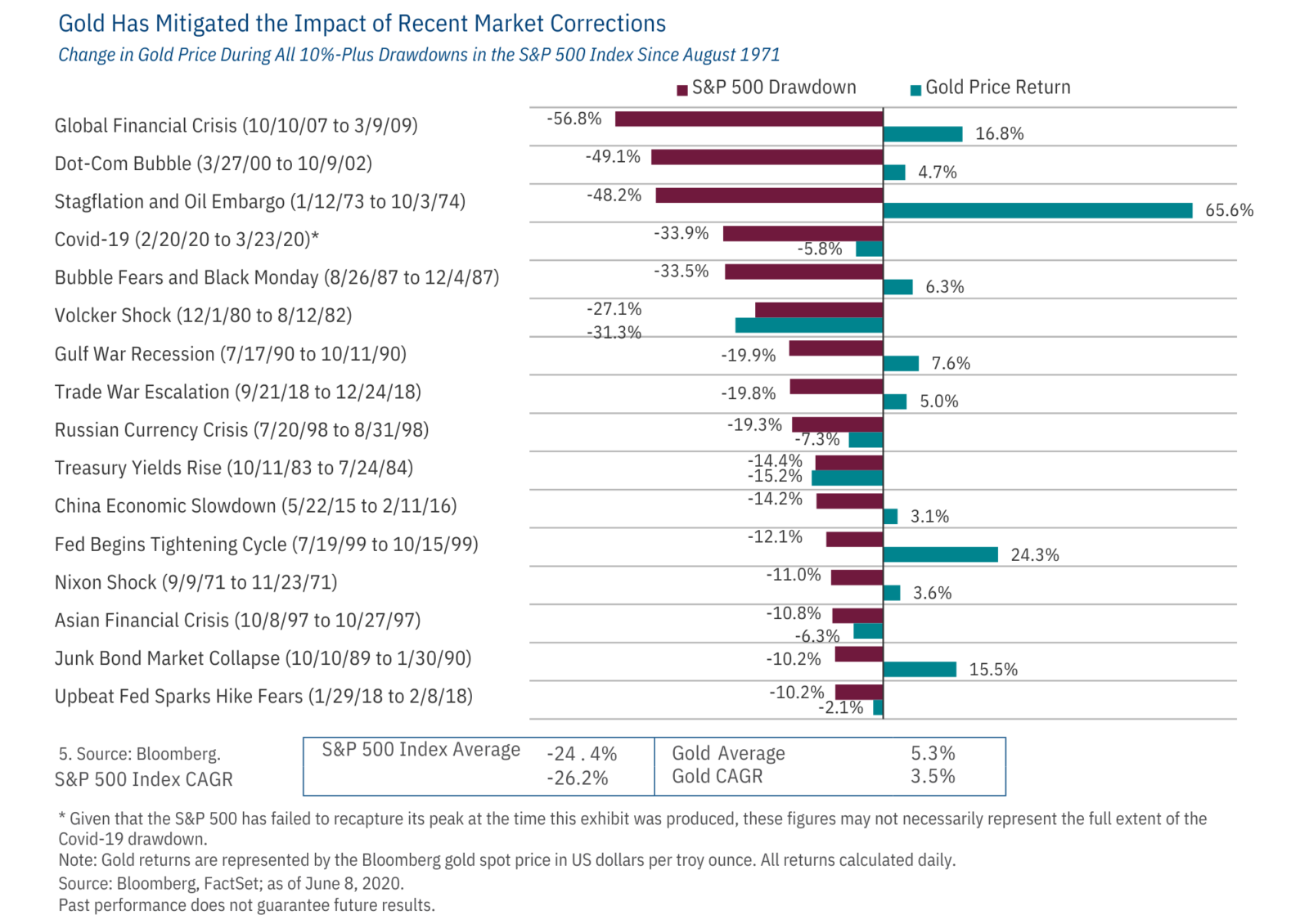

Disruptive financial circumstances are a threat model that includes sharp selloffs and heightened volatility in asset values due to unpredictable events, withholding the extreme example discussed in our first threat model. Historically, gold as an investment asset has served as a diversifying complement to equity portfolios under most periods of extreme equity market distress. The most vivid example for many investors today would be the Great Financial Crisis when gold gained nearly 6% in the calendar year 2008 versus the S&P 500 negative return of 36.55% [3]. As shown in the table below, gold outperformed the S&P 500 in 14 of 16 10%-plus drawdowns since 1971 and did so by a margin of 30% [4]. For these reasons, some view it as empirically important to always have a strategic allocation to gold which has a nearly zero average long-term correlation to the S&P 500 [5].

Source: First Eagle Investment Management LLC, Insights August 2020

Fundamental valuation is also an important consideration when making an investment in gold. Gold does not produce any cash flows and has little industrial use, so deriving the intrinsic value or price of gold is largely determined by supply and investor sentiment at the time. Gold supply is fairly limited, which does provide a floor price to the asset, but again, the price is largely derived from what another buyer is willing to pay and can be widely influenced by a speculative narrative, which an investor has little control over and can quickly change without any notice. As shown above, gold tends to hold a higher perceived value during periods of heightened fear and financial distress. If disruptive financial events hold a high value in your threat model, an allocation in gold to your investment portfolio between 5-15% may provide additional diversification benefits and help protect your capital. This investment allocation can be easily made through financial derivatives such as ETFs, futures, or an active manager which allocates gold as part of their investment strategy.

In conclusion, the radio and TV gold advertisements will likely never stop, but understanding your threat model and weighing how much this threat means to you can help you determine if owning gold is right for you. Gold can be held either in the physical form or in your investment portfolio. In the unthinkable, physical holdings of gold may bring comfort. Additionally, gold as an investment has some merit during periods of extreme financial distress but is less effective as a hedge against inflation. It is important to remember gold is only one investable asset in the investment universe. Just like your nutritionist might tell you, “A healthy diet has lots of color,” a healthy investment portfolio should have lots of color to provide the full benefits of diversification. If you like everything you own or do not hate anything, you are probably not diversified and should consider consulting with your advisor. At Bridgeworth, we aim to build robust portfolios that are well-diversified to help keep our clients on the path to their goals.

Bridgeworth Wealth Management is a Registered Investment Adviser.

The opinions and information contained herein have been obtained or derived from sources believed to be reliable, but Bridgeworth makes no representation or guarantee as to their timeliness, accuracy, or completeness or for their fitness for any particular purpose. The information contained herein does not purport to be a complete analysis of any security, company, or industry involved. This material is not to be construed as an offer to sell or a solicitation of an offer to buy any security. Opinions and information expressed herein are subject to change without notice.

Investing strategies, such as asset allocation, diversification, or rebalancing, do not assure or guarantee better performance and cannot eliminate the risk of investment losses. All investments have inherent risks, including loss of principal. There are no guarantees that a portfolio employing these or any other strategy will outperform a portfolio that does not engage in such strategies. Past performance does not guarantee future results. There is no guarantee that any forecasts made will come to pass. Any securities, indices, and other financial benchmarks shown are provided for illustrative purposes only and reflect the reinvestment of income, dividends, and other earnings. They do not reflect the deduction of advisory fees. Investment products are subject to investment risk, including possible loss of the principal amount invested. You cannot invest directly in an index.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not ensure against market risk.

This content does not constitute legal, tax, accounting, financial, or investment advice. Any discussion pertaining to taxes in this communication may be part of a promotion or marketing efforts. As provided for in government regulations, advice related to federal taxes that is contained in this communication is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue code. You are encouraged to consult with competent legal, tax, accounting, financial, or investment professionals based on your specific circumstances. Sources:

[1] YCharts (2023). Gold Price in US Dollars (I:GPUSD)

[2] YCharts (2023). Gold Price in US Dollars (I:GPUSD), Bureau of Labor Statistics

[3] YCharts (2023).

[4] Source: First Eagle Investment Management LLC, Insights August 2020

[5] YCharts (2023)